Your Guide to Getting a Mortgage in the UAE

25 February 2026Written by Andre

As Dubai’s property market has surged over the past 15 months, there has been a significant demand from both local and international buyers looking to purchase new homes. While cash buyers are influential in driving the market, a substantial portion consists of those seeking to buy property in Dubai mortgage.

Mortgages, which were still something of a novelty in Dubai as recently as two years ago, have now become an integral part of the buying process in some cases. Anyone can get a mortgage, whether they are Emirati nationals, resident expats or even non-residents, and the process is relatively straightforward compared to other global cities.

How much can you borrow for a mortgage?

According to the UAE Mortgage Cap Law, expats and non-resident buyers need to make a down payment for at least 20% of the property value (15% for UAE nationals) if the property is priced at below AED 5 million. That amount goes up to 30% (25% for UAE nationals) if the property is more than AED 5 million, and 40% if the mortgage is for a second or third property.

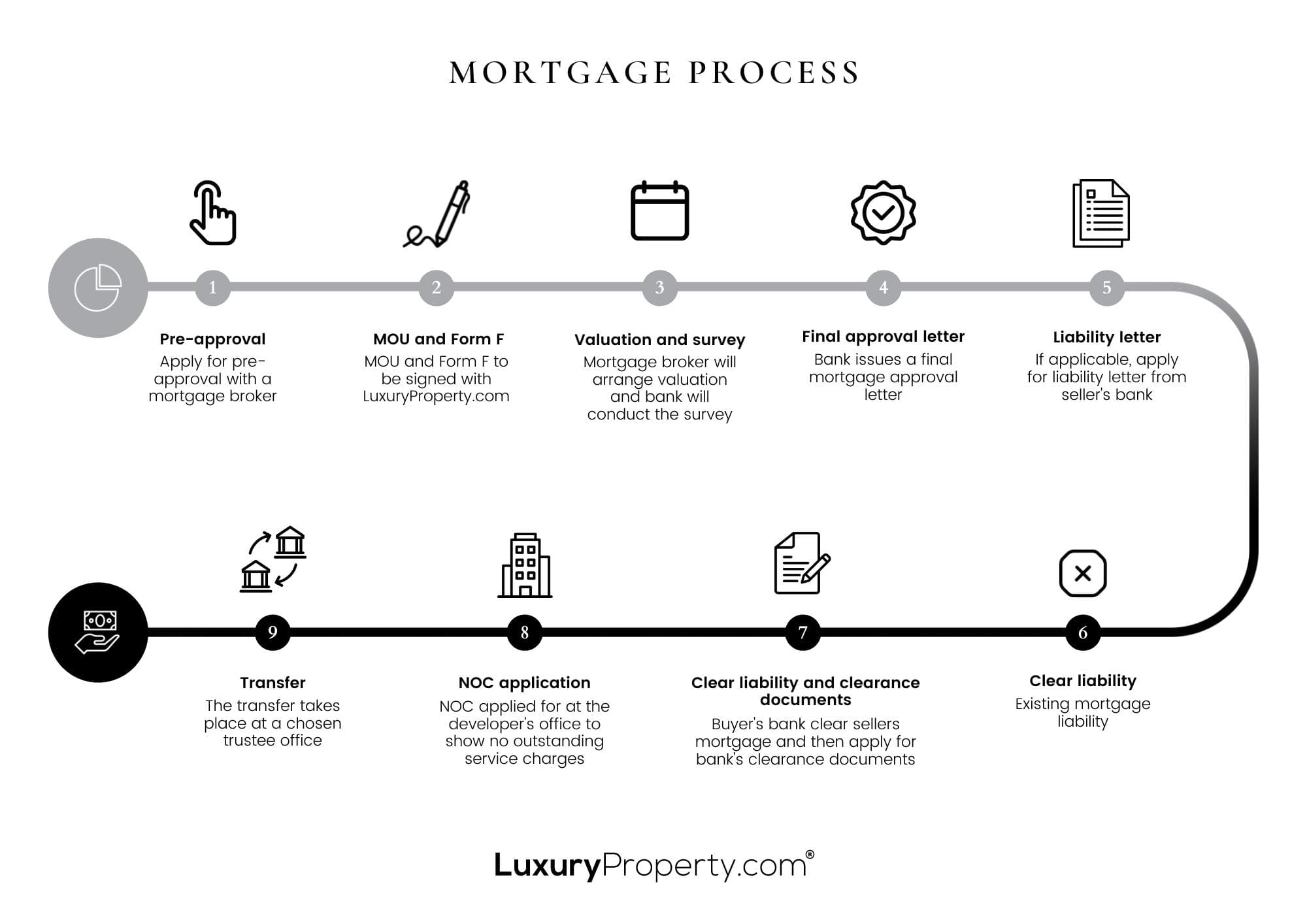

Once you have calculated your mortgage amount - with the help of an online mortgage calculator that is available on most bank and mortgage brokers’ websites - you need to apply for a pre-approval from the bank. Simply put, the pre-approval is an official agreement from the bank that your loan amount has been approved. We have covered the pre-approval process in a previous blog but in a nutshell, a pre-approval is valid for 60 days from the day it’s issued and it gives you peace of mind as a buyer, knowing that you will be able to get financing for the property you want.

What is the property buying process?

When a property purchase is finalized, the buyer and seller will need to sign a Memorandum of Understanding (MOU), or Form F (Sales & Purchase Agreement). At this point, the bank will conduct a valuation to determine the exact value of the property and the subsequent mortgage amount, following which a final approval letter will be issued.

If the property is currently under mortgage, the seller must obtain a liability letter from their bank, indicating the remaining mortgage amount. Additionally, a no-objection certificate (NOC) is required from the property developer, confirming that the seller has no outstanding service charge payments. This process is often facilitated by mortgage companies in Dubai.

The buyer and seller will then need to visit a trustee office in order to ‘block out’ the property in the buyer’s name, which will allow the buyer to clear the seller’s mortgage. In order to block the property, the following documents must be submitted to the trustee office:

- Liability letter from seller’s bank

- Form F (MOU)

- NOC from developer

- Copy of the title deed

- Cheque issued to seller’s bank for the amount stated in the liability letter

- Cheque issued to the seller for the remainder of the purchase price

- Cheque issued to Dubai Land Department for their fees (4%)

- Original ID documents of the buyer and the seller (Passport, visa and Emirates ID)

After the seller’s mortgage has been cleared and clearance documents obtained, the property can be officially transferred under the buyer’s name at the trustee office.

In order to ensure a smooth purchase and transfer process, it is advisable to work with a reliable real estate and mortgage partner. Our Private Client Advisory team is always available to assist you with any questions you might have about finding the right property in Dubai and to guide you through the buying process. We work alongside trusted mortgage brokers such as Mortgage Finder so you can get the loan that best suits your needs, with the best rates in the market. Contact us today to learn more.